Key messages and observations on the Asia Clean Energy Summit (ACES), October 24-25 are posted here. ACES is part of Singapore International Energy Week (SIEW) 2017.

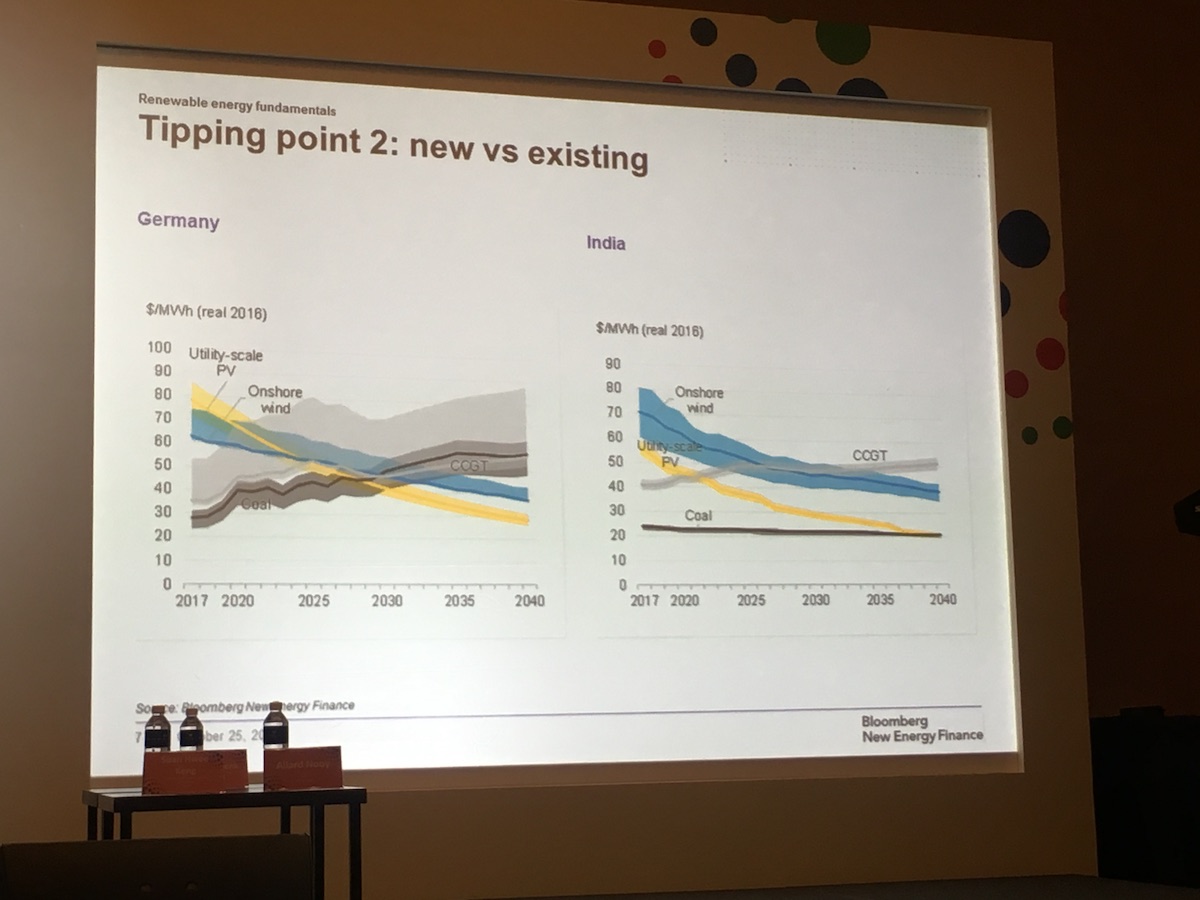

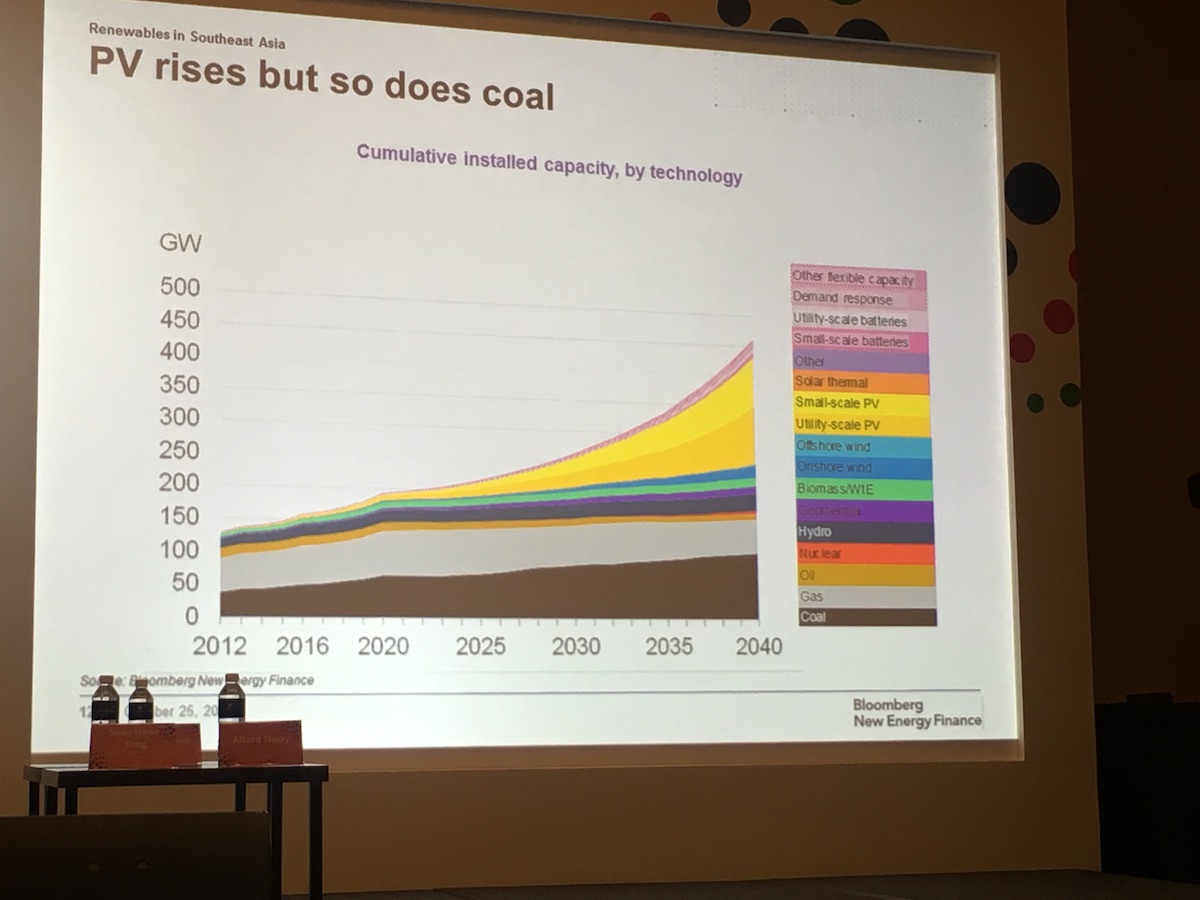

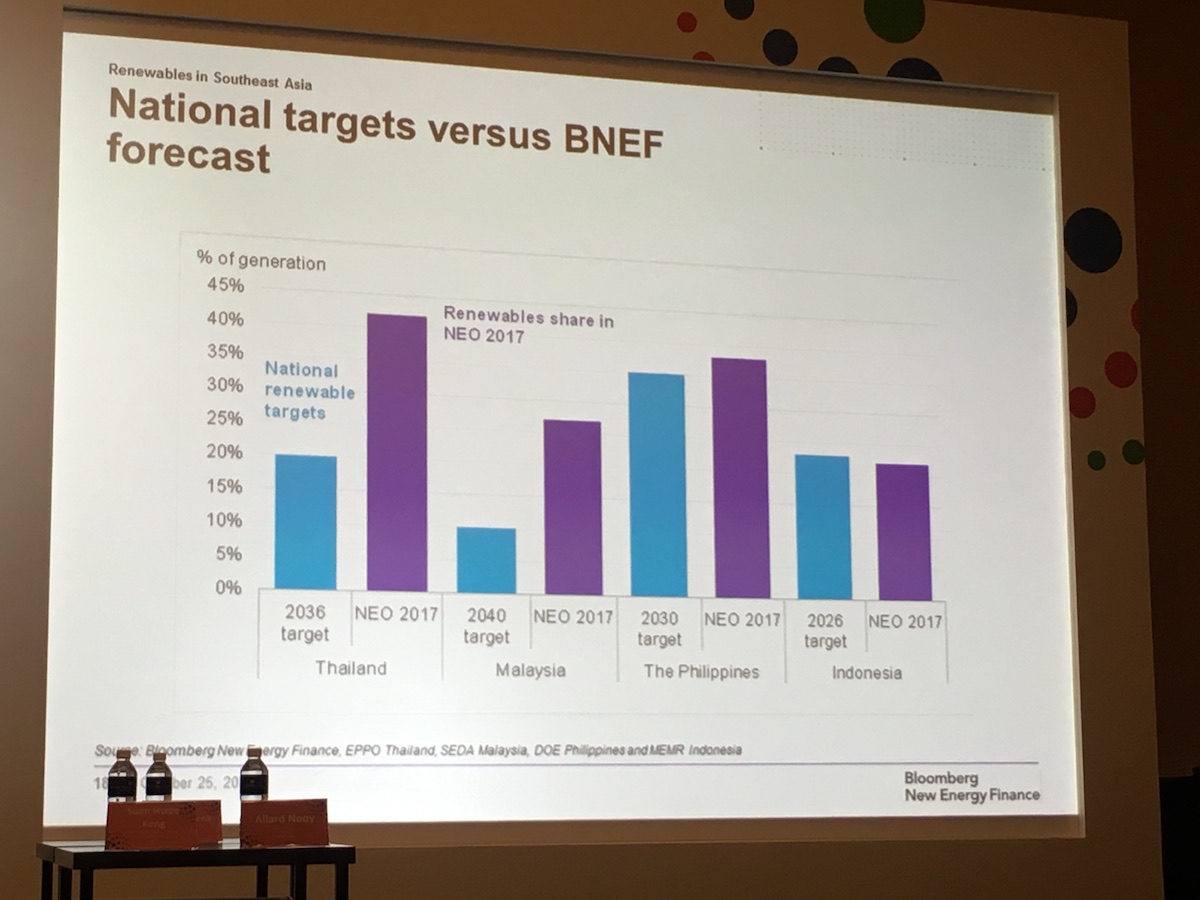

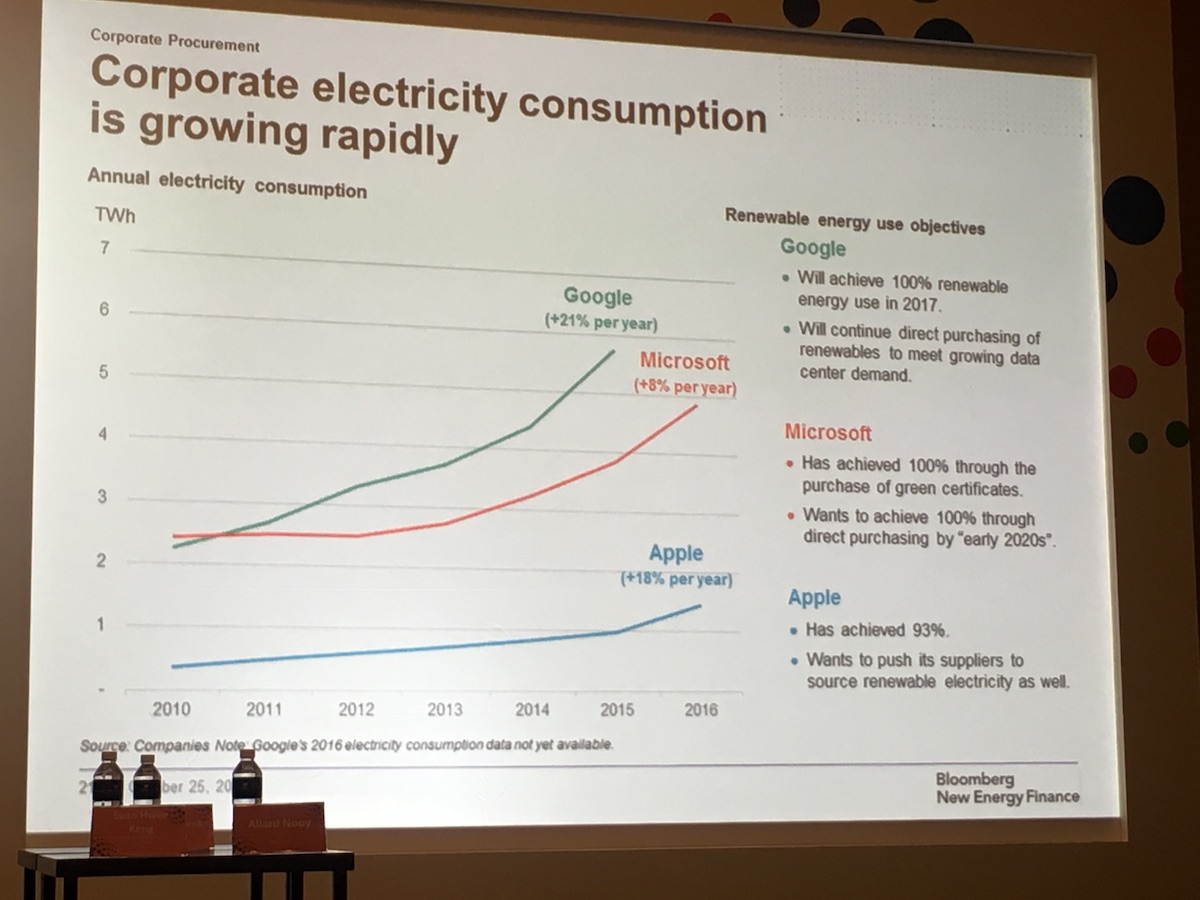

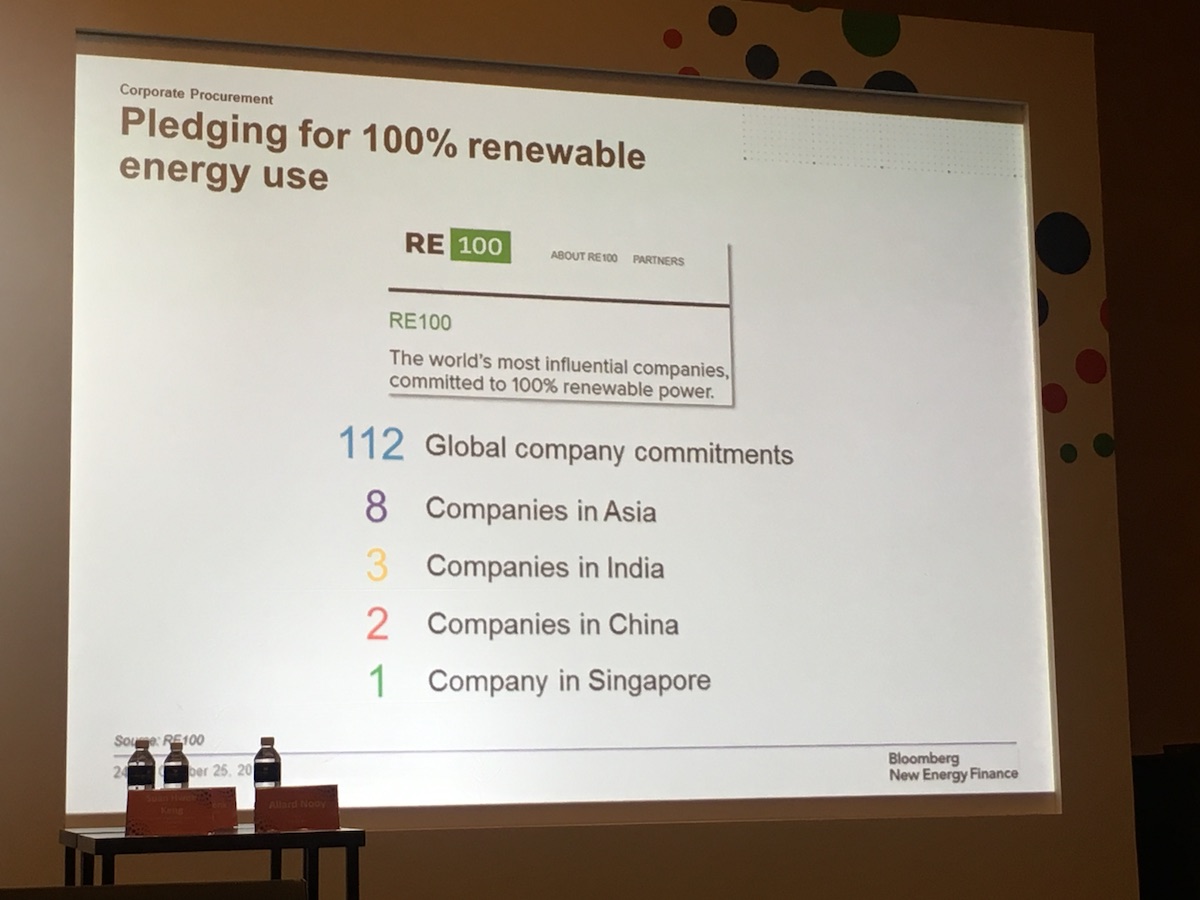

Day 2 of the Asia Clean Energy Summit started with the Financial Summit and was kicked off by Justin Wu of Bloomberg New Energy Finance, who gave a very insightful presentation on the Energy market. Key points were:

During the introduction of the session on the Energy Roadmap in Asia, Allard Nooy of Infraco Asia made the following key points:

The subsequent panel session addressed developments in financing of solar energy projects in Asia and raised a number of very practical points:

Share this article

Read Other Blogs

May 01, 2026 • Oil & Gas Industry

EnergyCC and CGD joint project conducted the preliminary scoping study on gas flaring and country trends

May 16, 2025 • Oil & Gas Industry

EnergyCC is working to reduce wasted gas emissions from oil and gas operations. It participated actively in COP26, COP27 and COP28 in collaboration with UNU-WIDER, to support the Global Methane Pledge. An overview of deliverables from publications, projects and events. Context EnergyCC is

Mar 30, 2022 • Oil & Gas Industry

This is the second of two papers delivered to UNU WIDER to address the global issue of global oil theft. This paper evaluates recent trends and commonalities of oil theft, describes potential actions and solutions to prevent oil theft, and mitigations against its consequences.